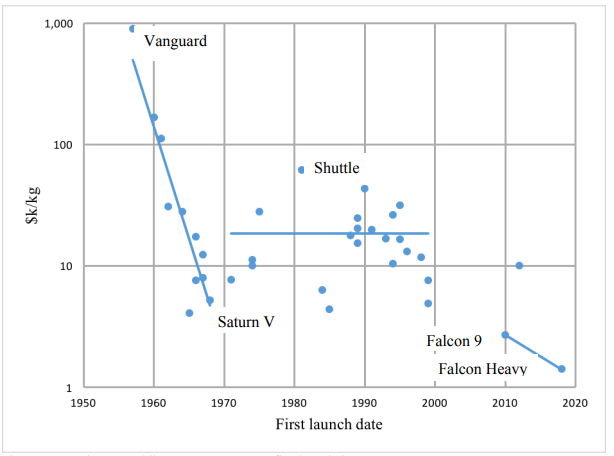

The International Space Station is the single most expensive construction ever completed. This is mostly because it is orbiting the Earth at around 400 km in outer space. Besides the complexity required of a structure hosting humans perpetually in an extremely unwelcoming environment, it cost a borderline unreasonable amount of resources to get the materials up to that height in the first place. The costs of space launch, after dropping exponentially in the early years of the Space Race, plateaued in the 1970s and were particularly high for NASA’s Space Shuttle program, the primary vehicle that lifted the materials we used to build the ISS. Though the numbers are a bit controversial, the Shuttle had a launch cost to Low Earth Orbit (LEO) of $61.7k/kg – this is much higher than the 1970-2000 global average that hovers around $18k/kg (Source). Shuttle was designed for both reusability and human crew, which ultimately drove up the total program costs.

Launch costs have gone through three periods of stasis or decay

In a nutshell, this is why SpaceX’s Falcon 9 and Heavy are such triumphant achievements – just in terms of cargo capacity, they’ve strode to a 95% reduction in the Shuttle kg to LEO costs, and are about 70-90% cheaper than other industry standards were in the early 2000s, like Atlas or Delta series launch vehicles.

As we move into the next few decades with exponentially cheaper access to space (not just LEO), there are no doubts that commercial, military, and scientific missions that would have been once prohibited entirely by the barriers to entry are now entirely feasible (or no longer laugh-out-of-the-roomable). For now, I’m particularly interested in discussing the commercial sector here, because not only are the hurdles for R&D and fixed investments lower, but the calculus surrounding marginal costs of working and building things in space has changed entirely. It’s obvious: instead of shelling out $100k+ for a single satellite, a company can deploy 10-20x as many for the same cost. And that isn’t even mentioning the scalability coming from software & hardware improvements and the network effects of services up and down the supply chain. Satellites are cheaper to make, and smaller too.

So the infrastructure for deploying hardware into orbit has gone (and continues to go) through a serious economic inflection point. Okay, what does that enable? What are the technologies and markets that we can stack on top of the orbital infrastructure layers?

The next step is probably manufacturing. If the fundamental hurdle for building things in outer-space is the cost of getting materials out of Earth’s gravity well, it makes sense that there is a primacy for figuring out how to harvest and utilize the effectively infinite (at the scale we currently operate, that is) resources within the solar system. But that’s a long way off, more on that later. It gets more interesting and real than that. Companies like RedWire’s Made-in-Space and Relativity are developing bleeding-edge manufacturing techniques that are geared towards such applications. But there is also the approach that is encapsulated by something like Jeff Bezos’s grand vision for space – off-worlding as much of the Earth-bound resource-intensive and ecologically-destructive activities as possible. In short, generating products and services for humanity, wherever it is, in space.

To date, we have NASA to thank for the most interesting work on the topic, laying out the feasibility of something like manufacturing products in LEO. In the mid-nineties, the Shuttle flew on three separate occasions with the Wake Shield Facility (WSF), an experimental platform gathering evidence of the vacuum wake concept. The idea was that pressure on the “wake side” of the platform could be decreased by ~6 orders of magnitude from the typical ambient pressure in LEO, around 10-8. It was found that the pressure decrease was only about 2 orders of magnitude, but the WSF was hailed largely as a success for something else: the WSF demonstrated the space epitaxy concept by producing gallium arsenide (GaAs) and aluminum gallium arsenide (AlGaAs) depositions (Source). I won’t get into it here, but GaAs semis are traditionally much more intensive to produce than silicon chips and offer significant benefits for niche electronics, such as high-speed digital circuits and LEDs or high-efficiency solar panels (Source).

Why microchips? Name a higher value per mass product whose fabrication requires vacuum levels on the order of <10-7 torr and a contaminant-free environment such as that found in outer space. The equipment required to produce vacuum is large and removing these systems could reduce deposition equipment mass by 48-72%, volume by 37-59% (Source). The contamination of an Earth-environment requires on the order of 1,000 gallons of ultra-pure water per wafer (or about 100 per chip) (Source), other consumables, and high maintenance demand. Stuff the WSF (mostly) didn’t require. The WSF also demonstrated that throughput and film/etching quality was increased, though not by any orders of magnitude. There are other immediate opportunities for flexing our manufacturing prowess in orbit, such as Zblan – a highly efficient fiber-optic substitute that simply cannot be produced at scale on Earth – and artificial organs – which researchers are working to demonstrate – but the synergistic effects of an orbital-based manufacturing stop for an already existent and massive terrestrial supply chain are too good to pass up.

The most interesting organization working on this opportunity right now is Founders Fund backed Varda, led by Will Bruey and Delian Asparouhov. Varda seeks to be a manufacturing and logistics platform for the in-space manufacturing of materials that are quality-dependent on the vacuum and microgravity conditions. The idea is that if the launch cost is low enough and the value of the materials that a space manufacturing platform can produce is high enough on a per unit weight basis, then there’s a point where the operations can be scaled such that profitability trumps that of such operations on the ground. While everyone else is seemingly focused on rapid, new-age manufacturing for space operations, Varda is dialing in on space manufacturing for Earth first.

It’s certainly a novel and bold idea; obviously with $53M in venture funding from Khosla, Lux Capital, Founders Fund, General Catalyst, etc., lots of terribly smart people think that it has legs. The narrative that’s easy to pick up here is: launch costs are decaying, more in-space activity is worth it now. I agree, but I wanted to see what it would take to truly do something like this successfully.

Economics of Varda

There are two ways of thinking about Varda’s cost curve. The simple way is to only attend to the variable cost of launching a platform and how much value that platform can produce. If it’s a fraction of a % more efficient at turning some raw materials into some (expensive) product than anything else, the in-space manufacturing is worth it. The more complex way is to factor in the development costs, capital requirements, and think about the marginal profit of each incremental satellite.

Also, for the sake of this analysis, I’ll be making assumptions based on the idea that Varda will be operationalizing a step or two in the semiconductor manufacturing process. This is for ease of comparison to an established market on Earth, but also because it is one of the more well understood in-space manufacturing activity and likely one of Varda’s first targets.

First, the relevant cost drivers:

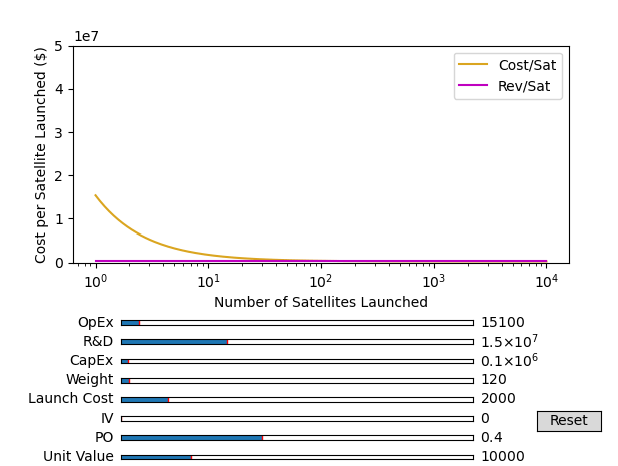

Launch cost ($/kg) [LC] – An obvious driver I discussed in the introduction, this variable traditionally represents a significant hurdle for in-space R&D. Optimistic forecasts put kg to LEO costs 10x cheaper than current prices around $2,000 by the end of the decade, primarily contingent on Starship development.

Operational Expense ($/sat) [OpEx] – This represents the cost of running a single satellite manufacturing hub for the amount of time needed to yield full production. This number is likely to be fairly low, but we can consider the material expenses for wafer manufacturing to be included here too. Dependent on the node size, wafer prices can vary from $16k to $5 – TSMC capital consumed for lower-end process nodes in 2020 was around $400, so we’ll assume ~$100 for anchoring deposition & etching costs (Source). It will also be much higher if these orbit manufacturing platforms are partially expendable, though Varda is of course tight-lipped about this. A university-developed satellite typically costs about $30,000, with the majority of this representing communications capabilities. For the sake of calculation, I’ll assume that the satellite is 50% reusable – this turns out to be a big unknown, but the payload has to return to Earth somehow. This gives an estimate around $15,100.

R&D spend ($) [RD] – This represents the program cost of designing and developing a satellite manufacturing platform for semiconductor production. Another tricky number with some nonlinear effects – R&D spend will step up periodically as a function of the number of satellites produced – but for the sake of calculation, I will simply use a run rate of the 1994 funding for the Space Vacuum Epitaxy Center, or Wake Shield Facility, which was about $5M. The entire program cost was around $15M, surprisingly low for a space experiment (Source). Varda has already raised $50M+ from seed rounds alone, so there’s a lot of room here or on the CapEx side of things.

Capital Expenditure ($) [CapEx] – This is the fixed cost of the satellite manufacturing hubs. I think this is a particularly difficult number to nail down, so for now I will simply use an industry average for Earth-based thin-film deposition machines. The high-performance Molecular Beam Epitaxy (MBE) machines for small scale production can cost around $1M while the most inexpensive of semiconductor deposition machines will run you about $75k. The efficacy of the hard vacuum in which LEO manufacturing will operate stands to lesson this cost load, but more on that in a bit. I’ll call it an ambitious $100,000 for now.

Now, the revenue drivers:

Payload optimization (%) [PO] – This is a ratio of the weight of the products after a full manufacturing cycle to the weight of the satellite (including raw materials). This metric can never be greater than 100%, and practically, likely never greater than 50% — the equipment mass, while smaller than that of terrestrial operations, is still substantial for even the simplest steps of the semiconductor manufacturing process. To ground the assumptions here, terrestrial MBE machines are huge, on the order of 1000 kg. Varda is aiming to return around 100 kg to Earth.

Number of satellites [S] – This number drives the economies of scale for an orbital manufacturing platform, as an increased number of satellites will drive R&D and fixed costs non-linearly and will amortize these costs across a greater number of platforms.

Unit value of product ($/kg) [UV] – The per mass value of the manufacturing product. 200mm 0.75mm silicon wafers are around 50g. Gallium arsenide substrates are about 50% heavier at ~5 g/cm^3 (Source). For something manufactured in orbit, a high unit value of product is extremely desirable as weight is a large cost driver. GaAs production is not as far along as silicon chips, so it is a bit unfair to compare the cutting-edge 8” wafers (GaAs to semi cost ratio of about 1000:1). For the smaller wafer sizes, GaAs are roughly 5-10x more expensive than silicon chips, depending on who you ask. Though I couldn’t find wafer and node specifications from the WSF, I don’t think it is too much of a reach to think that orbital manufacturing might soon allow these larger wafers to be produced at scale. If I assume a mean price of around $100 for a 200mm silicon wafer and a conservative 10x cost ratio, I get around $13k for a kg of GaAs semi wafers. Note this is the price of a completed wafer, and it might be the case that not all the deposition/etching process might occur on an orbital platform.

Incremental value of space-operations (%) [IV] – This is a weird metric I kind of made up for the purposes of comparing terrestrial manufacturing processes to those in orbit. A lot of the assumptions I am making, especially considering unit value and equipment costs, are grounded in terrestrial norms, which the very type of manufacturing I am considering seems poised to disrupt entirely. This means I am erroneously implicitly considering terrestrial cost to yield/quality ratios. Therefore, this IV number can be thought of as either or both 1) the improvement in % yield of semiconductors with given equipment (perhaps the equipment I’m pricing based on terrestrial manufacturing is waaay more than we need to get a comparable yield in orbit) or 2) the improvement in product quality and performance. Basically, whatever allows orbital manufacturing to sell a kg of product for more than it is currently thought to be worth with terrestrial equipment is considered IV. I don’t expect this to be much greater than 10%, as market pressure on the manufacturer is likely to allow them to underprice current production and attract a higher number of buyers for their service.

The weight of the satellite [W] is also an important variable that shows up as both a cost and revenue driver, and has some fun non-linear effects on the cost curve. Varda satellites seem to be weighing in around 120 kg so far, but that’s only for the initial test launches (Source).

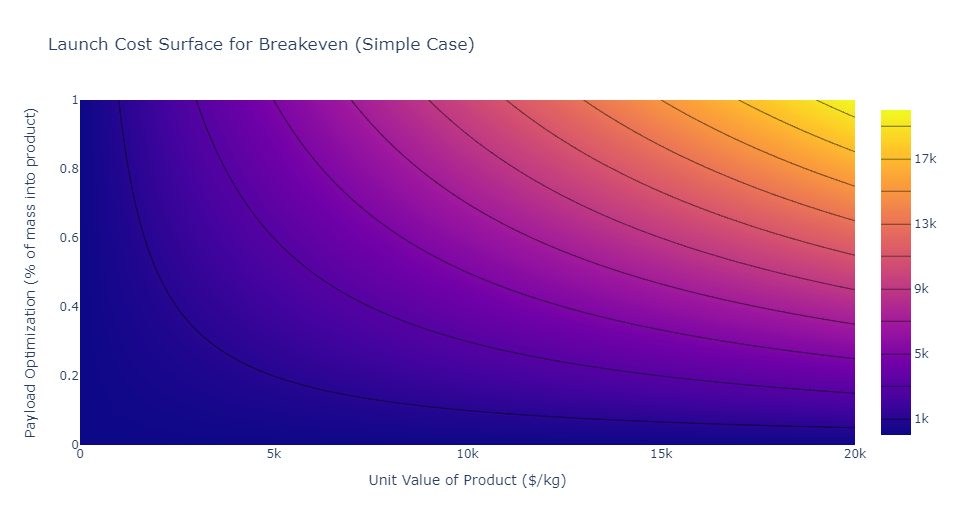

In the simple case, we are only concerned with three variables: Launch cost, payload optimization, and unit value of the product. The equation is shown:

The payoff here is independent of the satellites and their unit weight. We can see the launch cost surface for breakeven below:

What is above is a contour of the three-dimensional breakeven surface for launch costs. Given the parameters on the x and y axis, this shows what the maximum launch cost could possibly be to allow an orbital manufacturing project to breakeven. It’s clear here that the breakeven point rather recently came within feasible bounds ($2-10k launch costs) for realistic products in the $20k or less range, which is why we are having this discussion in the first place.

Okay, but what about the other variables in the equation?

“The future is showing that we can send the materials and the factory up to the space for 1 million dollars and we can make a million and one dollars of profit. [T]he moment that happens, we [will] turn around like SpaceX and start producing these factories every single day and make them larger and larger, where initially, rather than having something the size of the Photon, we have something the size of a school bus, and eventually something the size of the ISS, or even ten times the ISS.”

Asparouhov is referencing what I’m calling the simple case here. Yes, it would be incredible to show that semi manufacturing is even marginally more efficient on orbit, which you can then scale up and cash in. The problem is you then have to pay for everything required to scale it. And if you haven’t factored all these costs, like operational expense, into your initial profitability estimate, you could be in trouble. I’m not saying Varda is guilty of this, but most of the narrative around orbital manufacturing is. What I do think Varda is actually in danger of is that you might actually need something the size of a school bus (as opposed to a 120 Kg satellite) to produce enough to offset the operational expense of sending complex hardware to space.

Obviously, while Varda is trying to prove itself, it must focus on developing the most efficient (not necessarily the lightest weight!) way to produce the most expensive product it can — provided it has a large enough market to justify the spend required for such development. This brings me to the second lens through which we can analyze in-space manufacturing platforms, which incorporates a more exhaustive version of the cost & payoff curves. I’ll refer to this as the complex case, referring to an analysis of the entire lifetime potential of the project. Not a very traditional way of valuing things, but I’m curious and was definitely not in the mood to discount any cash flows so what the hell.

In the complex case, we exhaust the cost drivers and take a more granular look at revenue drivers.

Our breakeven point is

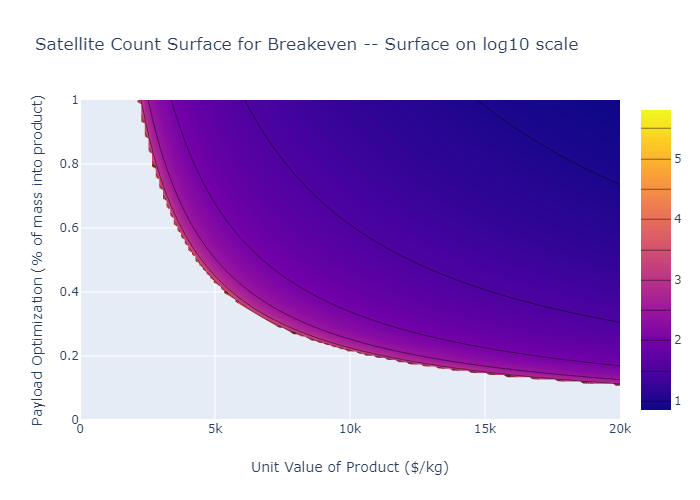

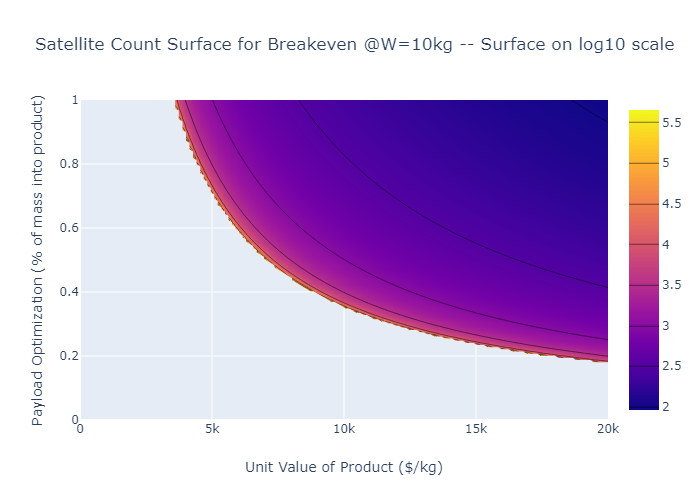

It’s a bit more practical to show this breakeven surface in terms of the number of satellites that must be launched in the lifetime of the project, as opposed to the launch cost. This is mostly because launch cost is actually a pretty well-predicted variable, at the moment. The others? Less so.

Overall, the landscape of breakeven launch costs for a satellite counts and weights looks like this:

Here’s what it looks like for PO and UV. The surface is on a log scale, so the 3 means Varda needs 10^3 satellites to break even. At some pretty conservative estimates here, we see that Varda needs ~100 satellites to break even. Not bad at all…

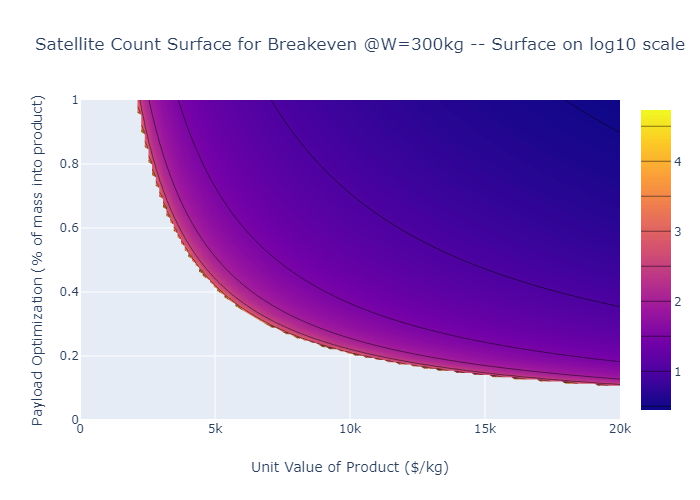

Here’s how it changes if we change the weights of the spacecraft.

There are immediately diminishing returns on the weight increase around 200 kg. Seems like Varda might have already done this analysis. But this diminishing effect is bounded by the launch cost of this weight. If launch costs get even cheaper, bigger is better.

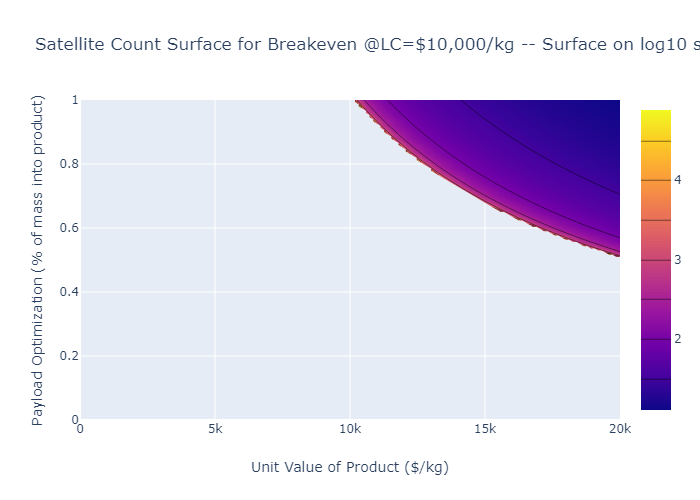

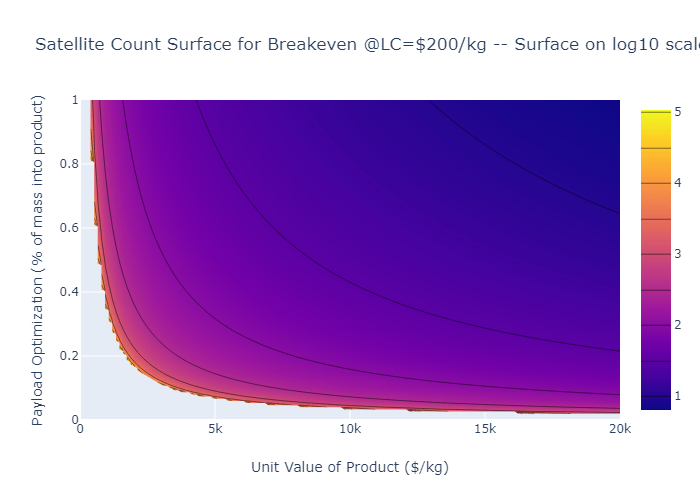

Here’s how the breakeven surface changes if we play with the launch costs.

There are two things of note here – the lack of diminishing returns on launch cost decreases (something Varda doesn’t really control) and how the surface simply disappears out of reach (for semi manufacturing, at least) when we go just a few thousand a kg higher.

None of the interactivity could be embedded on WordPress, but here’s a link to my git repo where you can play with all of these parameters and display the graphs above and below. Please check it out!

Briefly, what this means for Varda

There are a few neat insights I gleaned from my crude analysis here. Crude because R&D costs change per incremental satellite dramatically, different satellites make different products, etc. I’m accounting for basically zero nonlinearities here, so take this all with a grain of salt.

That being said:

- Opex matters very little.

- This is because launch costs are relatively huge. High OpEx can more than easily be offset by heavier satellites with better PO/UV. If Varda has to pay $30,000 to repair/replace every factory, it ends up being “so what.” I think that says a lot about how resource intensive a) Launches to space are and b) semi manufacturing is

- There are diminishing returns on increasing weight, but Varda should go for larger satellites as long as launch cost is below and/or PO or UV above a certain threshold (all three depend on each other)

- If making a satellite heavier even marginally increases PO or UV even less than it marginally increases capex or R&D, it’s probably worth it. This really only works with heavier satellites though, which means more throughput. R&D expense going up? Fine. The satellites just need to weigh more & be more efficient.

- There are basically no diminishing returns on launch cost.

- Think this is interesting, and it might be market forces working against Varda’s favor. They can make their satellites heavier, but that’s only as effective as launch providers make launches cheaper, something that offers diminishing returns to the launch providers (though Elon’s business case for Starship begs to differ).

- R&D order of magnitude increase scales roughly with total number of satellites to be launched.

- If Varda increases their R&D or CapEx spend by an order of magnitude, there is a roughly corresponding order of magnitude increase in the number of satellites required (at least in the 1-1000 satellites range). These are complex launch vehicles – I think it is obvious that the business case hinges on launch costs coming down even more, possibly even an order of magnitude.

Bottom line: If Varda has to make bigger satellites to make them more efficient at producing things, it doesn’t really matter. If launch costs stay below a certain threshold, heavier satellites actually help them. Operational costs don’t really matter, but launch costs by a few $100s per kg can make or break the business case if the Unit value of the product isn’t relatively expensive ($10k+/kg). If Varda can show that orbital manufacturing processes can produce something in this territory, returning even 35% of the weight launched in product, it won’t be too tough or capital prohibitive to scale to the ~1000 satellites required.

If semis don’t pan out, there are the other products that are somewhat flashier I mentioned earlier – Zblan and artificial organs, even run-of-the-mill clean-room procedures might be up for grabs in a low-launch cost future market.

If manufacturing doesn’t pan out, it might be that highly energy-intensive computing or solar harvesting processes might be best off-worlded to these platforms. It might even be the case then that they need to orbit the sun, or another planet, rather than home.

Where is the value in Space, actually?

It seems that LEO manufacturing of materials shipped off Earth is doomed to be constrained to a pretty small slice of the manufacturing pie. The highest value processes up there will be somewhat niche. What is a bigger deal is the value of these (conceivably) automated platforms and the scale that outer space (beyond orbit) enables. This is something that I think the SpaceX/Mars stans miss. A trip to Mars is simply a trip to Mars. At some point, even a non-profit-driven entity has to create tangible value (see: we stopped going to the moon & we’re crashing the ISS in a few years in favor of for-profit space-stations). The trips to the Americas in the 1400 & 1500s were funded explorations not for the sake of exploration, but for $$$. This point is almost too obvious to make, but something like human travel and settlement of deep(ish) space is a multi-trillion dollar endeavor. It has to be worth something tangible or it will fizzle out, if it even happens at all.

This is why Varda and other orbital infrastructure platforms are exciting. Yeah, they might be at the mercy of launch providers and doomed to keep up with terrestrial efficiency at scale, but the resources of deep space combined with the exponential nature of a manufacturing platform that could contribute to making more manufacturing platforms combined with the lack of a common resource to overburden (I’m talking about orbits above GEO now) is something that completely alters the paradigm of industrial innovation as humanity has known it until now.

This is the natural evolution of orbital manufacturing platforms. Entirely autonomous platforms capable of generating any specialized output; what we can make here on Earth and more, even more of themselves. Mass and energy are practically no longer constraints if we are talking about something like a platform that orbits the sun and strip mines Mercury.

Of course, this is in the far future, but so once was a handheld computer. It is only a matter of time before resource utilization in space becomes the ultimate market force, thanks to the launch cost decay brought on by commercial markets and the internet – if anyone is seriously planning on going to Mars, they should seriously plan to develop simultaneously autonomous manufacturing infrastructure that scales on its own. That is what a $10T project requires and so far, Varda & the likes (Made in Space, to name another) are barreling down the right direction.

Addendum

Find Code here for interactive charts!

Zblan showing promise…in 1998

Artificial organs in space, something I didn’t even cover really. Techshot and other companies are already building here and the IV here would break every chart in this post.

What does semiconductor manufacturing and spend look like at scale? TSMC is a great case study.

Bleeding edge wafer costs over the years

Don’t be blown away by cutting-edge semiconductor manufacturing. The hard part is the scale.

The Starlink project cost about $5B, for ~4,000 satellites. Moving to Mars would cost…$100K? Okay fine, but why would you go?

“The greatest value of the Moon lies neither in science nor in exploration, but in its material.” School of Mines, in particular, does better work than I on this subject. Check out Sowers in particular, he has some good cost-analysis of a cis-lunar economy.

Leave a comment